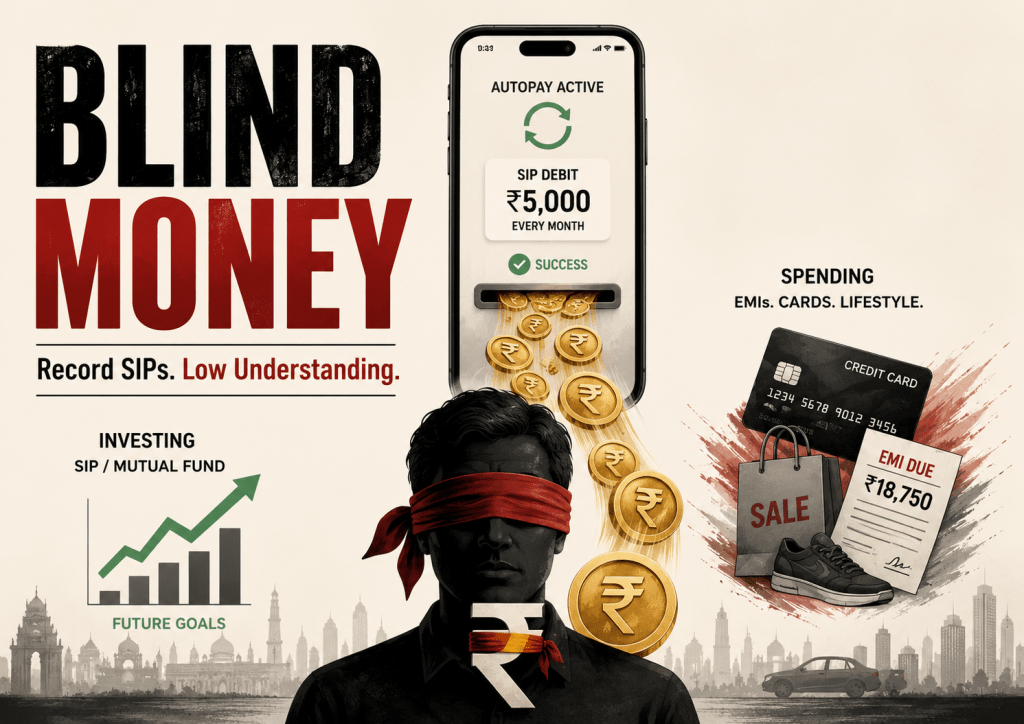

Blind Money: Why Record SIP Numbers Should Make You Nervous, Not Proud.

The SIP Paradox: India is investing more than ever and understanding less than ever.

In 2025, cumulative annual SIP inflows crossed ₹3 lakh crore for the first time, according to AMFI data as reported. Then in early 2026, monthly SIP collections touched roughly ₹32,000 crore in a single month.

That sounds like progress.

But here’s the uncomfortable part. A country can invest more money and still understand less about money.

That is where the danger begins.

Because record SIP numbers do not automatically mean record financial wisdom. They may simply mean millions of auto-debits are running on time while the people behind them have no clear idea what they own, why they own it, or what they will do when it falls.

Let’s be honest about this. India has become very good at starting SIPs. That does not mean India has become financially literate.

The SIP Is a Tool, Not a Brain

A SIP feels intelligent because it is automated.

Money leaves your bank account every month. It goes into a mutual fund. You feel responsible. You feel adult. You feel like you are building wealth quietly in the background.

That feeling is powerful.

But the SIP itself is not a strategy. It is just a mechanism.

A Systematic Investment Plan does one simple thing. It puts a fixed amount into a selected mutual fund at fixed intervals. That is it.

It does not guarantee returns. It does not protect you from choosing the wrong fund. It does not know your goals. It does not understand your risk capacity. It does not care whether you need the money in three years or twenty years.

Before the auto-debit starts, the questions should be obvious. Why this fund? What is my time horizon? What would make me stop?

Most people never ask.

The SIP is like an auto-debit instruction with better branding.

Useful? Yes.

Magical? No.

Most people treat the SIP like a financial vitamin. Take it every month, do not think too much, stay healthy.

That is not investing. That is outsourcing thought.

From Fixed Deposit Blindness to SIP Blindness

A generation ago, the Indian middle class had one default answer for surplus money.

Put it in an FD.

Why? Because parents said so. Because the bank felt safe. Because the number was guaranteed. Because nobody wanted to think beyond interest rate, tenure and maturity value.

Very few people asked whether the return was beating inflation. Very few asked what tax was doing to the real return. Very few asked whether their money was actually growing or merely sitting politely in a bank’s ledger.

Today, the product has changed. The blindness has not.

Now the default answer is different.

Start an SIP.

Why? Because influencers say so. Because the app makes it easy. Because everyone on social media says consistency beats timing. Because the word “equity” sounds smarter than “fixed deposit.”

But the real questions are still missing.

What am I buying? Why this fund? What does this fund own? What is my time horizon? What happens if this falls 30 percent? Am I investing for retirement, a house, my child’s education, or just because the app showed me a chart moving upward?

The wrapper changed from FD to SIP.

The thinking did not.

That is the real problem.

The Literacy Gap Nobody Wants to Discuss

India’s investment numbers look impressive. The literacy numbers do not.

Reporting tied to the National Centre for Financial Education has placed basic financial literacy among Indian adults at roughly 27 percent. Some reporting places financial literacy among millennials even lower, around 19 percent, despite high confidence in their own money knowledge.

That gap matters.

Because confidence without understanding is expensive.

Now add another layer. India’s Gen Z reportedly accounts for around 43 percent of consumer spending. This is the same generation tapping phones for everything: food delivery, fashion, travel, gadgets, subscriptions, EMIs, credit cards, BNPL and also SIPs.

Look at the contradiction.

The same person may have a monthly SIP running for retirement and a no-cost EMI running for a phone that will lose half its value in two years.

The same person may be investing in equity funds while paying credit card interest.

The same person may be proud of “starting early” while having no emergency fund, no debt framework, no asset allocation and no idea what their portfolio actually contains.

Without a framework, money behaviour becomes fragmented. SIP for future. EMI for present. Credit card for lifestyle. BNPL for impulse. UPI for dopamine.

Everything is active. Nothing is integrated.

That is how people confuse financial activity with financial progress.

When Markets Fall, Blind Money Gets Exposed

Markets have a way of revealing who understood the game and who was just clicking buttons.

In early 2026, when markets corrected sharply, reports showed a clear divergence. Retail direct equity participation fell, while mutual fund holdings kept rising on the back of SIP flows.

On the surface, that looks like maturity.

Maybe it is, for some investors.

But not all staying invested is discipline.

Sometimes the SIP continues because the investor understands volatility, accepts drawdowns, and knows the time horizon.

Sometimes the SIP continues because the investor forgot it was running.

From outside, both look identical.

Inside, they are completely different.

One is deliberate. The other is accidental.

The person who understands their portfolio can hold, rebalance, add more or do nothing with intention. The person who does not understand simply reacts when the pain becomes visible. Until then, automation does the work and gets mistaken for wisdom.

This is where blind money gets exposed.

A falling market does not only test returns. It tests conviction.

And conviction cannot be automated.

If the market falls 30 percent, do you know whether you are supposed to continue, pause, rebalance, or rethink?

That answer should come from understanding, not panic.

Automation Without Understanding Is Still Sleepwalking

The Fiat to Free view is simple.

Real financial awareness is not about which product you use. It is about whether you understand the system you are participating in.

A SIP can be a powerful tool. But a SIP in the wrong fund, for the wrong goal, with the wrong time horizon, held by someone who does not understand risk, is not wealth building.

It is sleepwalking with an auto-debit.

The financial system loves this version of the investor. Regular inflows. Low questioning. High trust. Minimal understanding.

That is not ownership.

Ownership requires knowing what you own.

If you own a mutual fund, you should know what kind of fund it is. Equity, debt, hybrid, index, active, sectoral, thematic or something else. You should know whether it is meant for growth, income, tax planning or speculation. You should know whether the money is for five years, ten years, or thirty years.

You do not need to become a fund manager.

But you do need to stop treating your own money like someone else’s responsibility.

Because here’s the thing. Blind investing may feel safer than blind spending, but it is still blind.

And blind money always belongs to the system before it belongs to you.

The Question Your SIP Is Waiting For

This is not an argument against SIPs.

It is an argument against unconscious SIPs.

Investing is not the problem. Automation is not the problem. Mutual funds are not the problem.

The problem is the belief that starting an SIP means you have understood investing.

That belief is dangerous because it gives comfort before clarity.

A financial vitamin is useful when it is part of a real plan. It is dangerous when you keep taking it just because an ad, an app, or an influencer told you it is good for everyone.

The old middle class trusted the bank and called it safety.

The new middle class trusts the app and calls it discipline.

Both may be wrong if nobody is asking the harder questions.

So do not open your investment app just to check returns.

Open it and ask something sharper.

If this SIP continues for the next ten years, do I actually know what I am buying, why I am buying it, and what would make me stop?

Leave a comment